Why the shift to conversational insurance journeys isn't about what came before — it's about what's now possible.

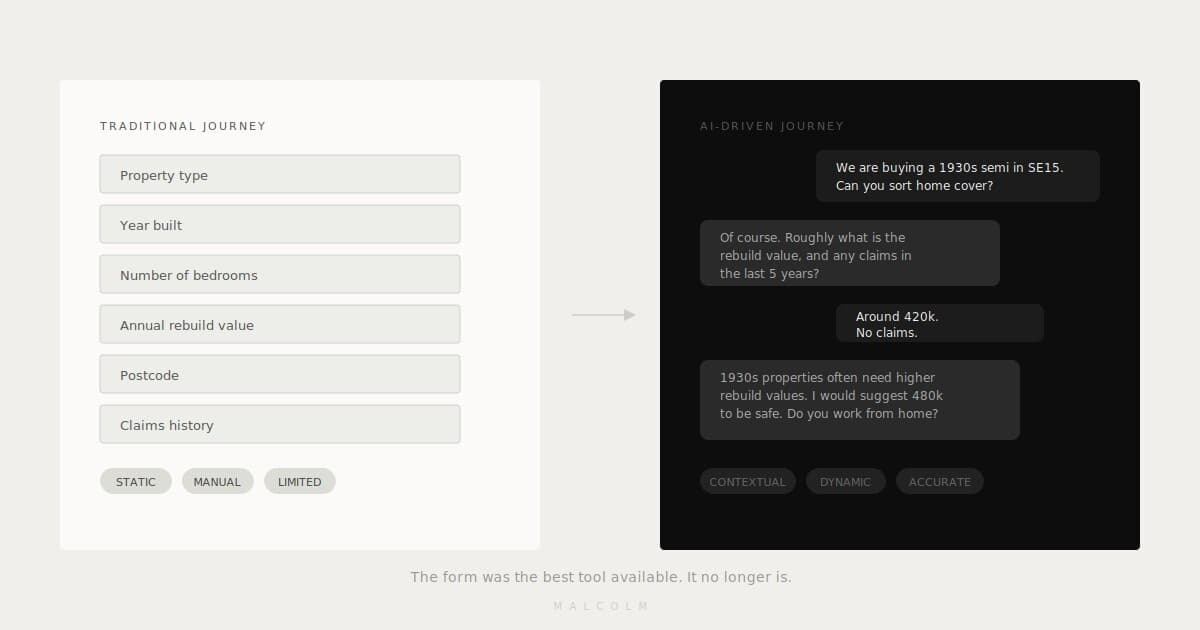

The digital insurance journey has been built on a form for thirty years. Fill in your property type, your rebuild value, your claims history - see a price, compare your options - buy!

And that worked, and still does in some cases. Digital distribution made insurance accessible, transparent, and competitive in ways that were not possible before. The form was the right tool for the channel it was designed for.

That said, the constraint on user experience and underwriting/pricing has always been information. A form can only capture what it asks for, and it can only ask for so much before the customer gets frustrated or confused.

What a form can and cannot capture

To state the very obvious, the questions a form asks are, by necessity, standardised. They have to apply to every customer, every property, every car, every risk. That is what makes them scalable, but it's also what makes them rigid and limited.

For example, in Home insurance - a form asks for rebuild value. Most customers don't know their rebuild value, so they enter a number - usually the purchase price, or a rough estimate - and the journey continues. A form can't follow-up or clarify, really - and it can't intelligently clarify the ask. It also can't flag that the figure entered seems low for a 1930s semi in SE15. It can't ask whether there has been an extension, or whether the home office equipment in the spare room should be covered separately. It takes the input and returns a price - or doesn't!

From there, results are ranked by price - often considered the primary, if not sole, comparison criterion - and the user makes a choice. They go ahead to buy a policy which is hopefully right for them, but may well not be.

This isn't a flaw in how digital distribution was designed, it's an inherent limitation of the tooling that's been available to-date. The form was the best available mechanism for capturing risk information at scale and returning a comparable output.

The constraint is now changing.

What a conversation makes possible

A conversational journey doesn't replace the form with a longer form - at least when it's done well. It replaces it with something far more contextual, relevant, and streamlined - especially when the AI already has access to a lot of the user information needed to get a quote.

But more than streamlined, it's also a clearer experience. If a customer mentions they work from home, it can ask about equipment value. If the rebuild figure seems inconsistent with the property description, it can flag that and ask for clarification. If a customer is describing a risk that a particular policy excludes, it can surface that before purchase rather than after a claim. All of these dimensions are capturable intelligently when relevant, and omitted when not - all possible, but hard to do well in a conventional form.

From the insurer's side, we also need to consider that the questions customers ask in natural language can also be more revealing than pre-existing form fields can offer. For example, when someone types "I'm buying a 1930s semi and need home insurance" into an AI assistant, that single sentence contains more useful underwriting context than several form fields would capture. The year of construction, the transaction timing, the framing as a new purchase rather than a renewal - all of it's there, if the system knows how to use it. You can imagine plenty more examples which offer the opportunity to really understand a customer better than you can already (this clearly raises interesting questions about how, and what data can be used in a world of fixed pricing models).

Conversational journeys surface that information and apply it. The result is a customer who arrives at a product recommendation with more context about what they are buying and why it fits their situation. This might well mean a slightly more expensive policy, but it also means one that's actually matched to their needs.

Both dimensions matter

That's not to say price doesn't matter; it clearly does and always will. The transparency that digital distribution brought to insurance premiums was genuinely valuable, and nothing about conversational journeys diminishes that.

The argument is not that price is the wrong dimension - it's that it's an incomplete one on its own.

A policy that costs less but excludes the risk the customer most needed to cover isn't a better product for them - but at present, the customer doesn't necessarily know that at purchase. They find out when they claim. At that point, the savings on the premium are irrelevant.

Coverage, exclusions, and fit are as commercially important as price - to the customer, because they determine whether the product actually does its job, and to the insurer, because a customer who claims and discovers they were not covered is a much more costly outcome than one who paid a marginally higher premium for the right product.

Conversational journeys make both dimensions visible at the moment they matter: before purchase.

The infrastructure question

Customers are already using AI assistants to research financial products, compare their options, and ask questions about what their policies cover. This isn't a future behaviour, it's happening now.

The question for insurers is whether their products are present and accurately represented in those conversations, and whether the journey from conversation to quote to bind can happen safely, compliantly, and without requiring a rebuild of core systems.

That requires infrastructure designed for the format - one that can take a natural-language conversation and convert it into the structured underwriting data existing systems need, while maintaining the audit trail and compliance controls the regulatory environment requires.

The form was thirty years of distribution infrastructure. What replaces it needs to be built with the same rigour, for a fundamentally different input.

Malcolm is the infrastructure layer that connects AI assistants to insurer systems, enabling conversational insurance journeys that are compliant, auditable, and built around the customer's actual situation. Learn more at trymalcolm.com.